In October 2021, the Chinese government has decided on rolling out a pilot property tax in some regions within the next five years, before proceeding with formal legislation. Under the scope of “common prosperity”, the government aims at narrowing the wealth disparities that have been partially caused by the large gaps in homeownership. However, the socio-economic reform plan has ignited much debate on its possible impact.

China currently does not have a comprehensive property tax in place. A property tax has been pondered on by Chinese leaders since 2003. However, concerns about the tax’s potential damage on property demand and house prices, which would eventually trigger a fiscal crisis for local governments heavily dependent on land sales as income sources, halted the idea.

Within the last two decades, only Shanghai and Chongqing have trialled property taxes between 0.4% and 1.2%, targeting mainly second homes, luxury properties, and purchases by non-residents. The tax did not reap large benefits for the two municipalities, accounting for only 5% or less of local tax revenue in 2020. Meanwhile, more than 20% of the Chinese local and regional governments (LRGs)’ revenue comes from land sales to real estate developers.

According to Xinhua, the new property tax will be more extensive than its previous trials. The tax will be applied to both residential and non-residential property, as well as land and property owners. The only exception from the new tax is the legally owned rural land where residences are built on.

The property sector plays an important role in China’s economy. Property accounts for 70% to 80% of household wealth in China and drives approximately 10% of household income. Over 90% of households in China own at least one home, and over 20% of which own multiple properties.

China’s home prices have soared by more than 2000% since the privatization of the housing market in 1998. The unstoppable rise in prices has also sparked speculative purchases and frenzied construction, funded by massive borrowing.

China’s Property Market Is Representative of Its Growing Inequality

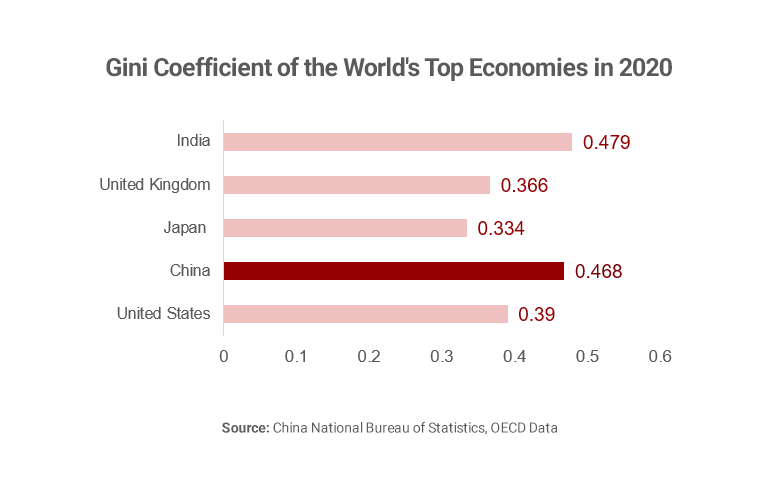

The income inequality in China has increased over the last few decades. The top 10% of the population earned 41% of national income in 2015, a wild rise from 27% in 1978. Meanwhile, the earning share of the lower-income half fell to about 15% from 27% in 1978 (Piketty, Saez and Zucman (2019)). China ranked second among the world’s top economies in 2020 in Gini coefficient – a measurement for inequality from 0 to 1, with 0 being perfect equality.

Property ownership is the biggest driver of regional disparities, the urban-rural divide, and inequality between urban households in China. The sector’s overloaded speculation has pushed up housing prices, widened the wealth gap, and suppressed residents’ desire to spend money elsewhere.

“Property tax in China is much more than a wealth distribution from rich to poor, but from older generations and high-tier city residents to the rest.” (Larry Hu, chief China economist at Macquarie). China’s privatization of the housing market in 1998 enabled older generations to purchase houses and apartments at a lower cost and to accumulate a larger share of property than younger generations. In recent years, the soaring prices have created an affordability crisis, especially among millennials.

The Multifaceted Impact of a New Property Tax

The new property tax would pose a great impact on the Chinese economy in both the short- and long-run. Pressures on the property sector and governmental revenue may significantly impact the country’s long-standing economic growth. At the other end of the spectrum, the property tax is expected to bring long-term sustainable benefits to both the local governments and its people.

1. Short-term pressure on the economic growth

Opponents caution that the property tax will likely chill the market and significantly shortcut China’s economic growth. According to Yue Su, principal economist at The Economist Intelligence Unit, if there are simultaneous property dumps, that might slow the introduction of property tax and increase the ability of individuals to apply for exemption (CNBC). The government will need to weigh the economic and social consequences of any moves on the real estate market.

2. Housing bubbles prevention

Proponents say the tax will prevent housing bubbles from getting perilously larger. The decline in the appeal of property investment could also divert private capital to other sectors, such as high-tech supply chain management and consumer services, which subsequently helps boost domestic consumption.

3. A long-term decline in interest rates

It is also expected that the tax, once introduced more broadly, will lead to a long-term decline in interest rates as construction of new homes will likely reduce and provide less support to credit creation, according to Hongta Securities Co. The real estate sector has been the most important driver of credit creation in the past. Li Qilin, the chief economist at the brokerage, said in a report on October 24, 2021, that the local governments have used land as a key source of collateral to borrow money and fund infrastructure, which in turn drove up home and land prices.

4. Sustainable revenue for local and regional governments in the long run

According to research group Capital Economics, an effective tax rate of 0.7% of the total property value would have generated 1.8 trillion CNY (282 billion USD) last year in China, compared to 1.6 trillion CNY that local governments generated in net revenue from land sales minus billions of dollars in land transfer expenses.

Aside from closing an expanding wealth gap, the property tax would help stabilize China’s fiscal economy in the long run. However, the threat of an immediate sharp shock on the economy remains. The government will need to take immense caution as it rolls out the taxation policy to avoid hurting its citizen and economy.

Read more about our consulting services.

The insights provided in this article are for general informational purposes only and do not constitute financial advice. We do not warrant the reliability, suitability, or correctness of the content. Readers are advised to conduct independent research and consult with a qualified financial advisor before making any investment decisions. Investing in financial markets carries risks, including the risk of loss of principal. Past performance does not guarantee future results.

The views expressed herein are those of the author(s) and do not necessarily reflect the company's official policy. We disclaim any liability for any loss or damage arising from the use of or reliance on this article or its content. ARC Group relies on reliable sources, data, and individuals for its analysis, but accuracy cannot be guaranteed. Forward-looking information is based on subjective judgments about the future and should be used cautiously. We cannot guarantee the fulfillment of forecasts and forward-looking estimates. Any investment decisions based on our information should be independently made by the investor.

Readers are encouraged to assess their financial situation, risk tolerance, and investment objectives before making any financial decisions, seeking professional advice as needed.