The semiconductor industry witnessed strong growth in the last few years due to skyrocketing demand in every industry that applies digitalization and automation; from automotive and consumer electronics, to ICT infrastructure and healthcare. However, the current supply fails to keep up with a sharp rise in demand while the pandemic is causing supply chain disruptions. The challenging semiconductor shortage is expected to continue in 2022 and even last until 2023. Both upstream and downstream companies are trying to address this issue in different ways with the target to balance supply and demand.

As societies shifted toward a more digital lifestyle during the COVID-19 pandemic, demand for electronic products started to rise. Now, as the second year of the COVID-19 pandemic has passed, lockdowns are lifting in several countries. Economies have reopened gradually and the demand for digital products continues to rise, which leads to a larger demand for electronic chips. Consequently, global semiconductor revenue reached an all-time high at 555.9 billion USD in 2021, an increase of 26.2% (YoY). This is equivalent to 1.15 trillion semiconductor units shipped throughout the year. The sales are predicted to further increase by 8.8% and exceed 600 billion USD in 2022.

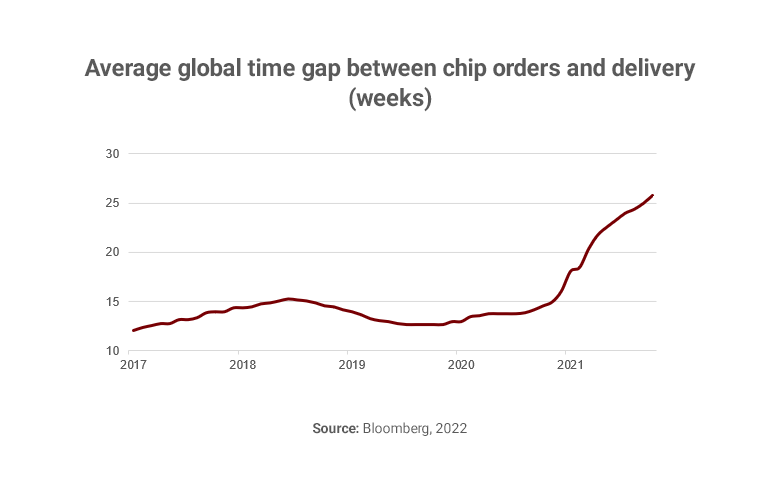

Despite suppliers’ efforts in pushing production to meet the demand surge, the semiconductor shortage remains a challenge to all industries that runs on these essential components worldwide. The global average delivery lead time soared 77% in December 2021 compared to the previous year, approaching staggering 25.8 weeks, according to Bloomberg. The long lead times have caused production delays, factory shutdowns, and revenue losses, especially for companies that have no buffer stocks. Acknowledging this issue, electronic chip-buying companies tend to place bigger order to mitigate the long lead times, which eventually amplifies the real demand, and worsen the current shortage while causing oversupply in the later period. Moreover, semiconductors manufacturers now concentrate on the production of the newest and most cutting-edge chips which are used in consumer electronics. Therefore, industries using “legacy nodes” or less modern chips like in the automotive industry continue to be the most heavily affected.

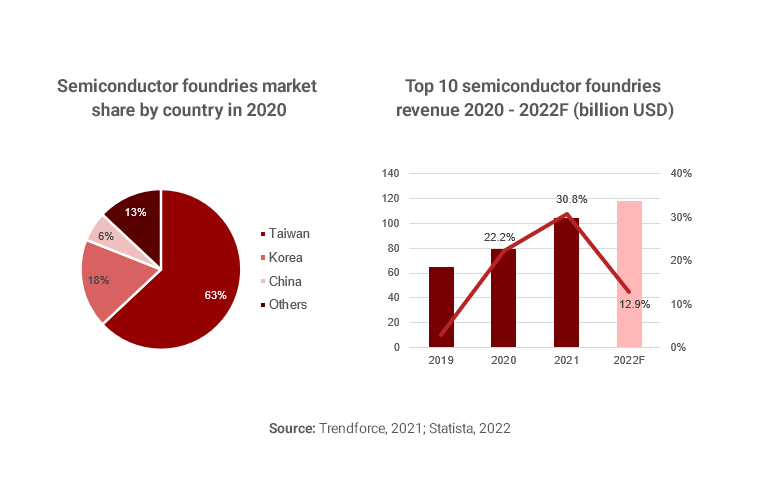

With the heaped-up orders in sight, semiconductor foundries, which are known as semiconductor fabrication plants, have significantly increased the utilization of their existing capacity since Q2 2020 and reached over 90% of the capacity in 2021. Revenue of the top 10 foundries grew dramatically by 30.8% in 2021 (YoY). The foundry market is projected to continue its growth by 12.9% in 2022. As of 2021, more than 80% of the semiconductor foundries were built in Asia Pacific countries including Taiwan, Korea, and China. Taiwan dominates the market, producing over 50% of the global chip production volume.

Hence, in order to catch up with the increase in demand, semiconductor manufacturers have invested in building new factories to expand their capacity. The world’s largest, Taiwan-based semiconductor foundry TSMC continuously announced ambitious expansion plans budgeting 100 billion USD through 2023, standing on the frontline of solving the chip shortage. For example, the construction of its 12 billion USD factory in Arizona was announced in 2021 and is expected to come into operation to make advanced 5-nanometer chips by 2024. Furthermore, it also plans to increase the capacity of the new factory in Japan, which focuses on producing chips with older technologies, but the production is expected to start in late 2024. TSMC has other expansion plans in Taiwan and Singapore as well. In addition, mainland China’s largest chip manufacturer SMIC also has aggressive plans to target self-sufficiency by building a 9 billion USD factory in Shanghai’s free trade zone.

Chip manufacturers are not alone in battling with the shortage. Chip-buying companies are also joining forces for expanding capacity as well as diversifying the supplier base and localizing production to mitigate their risks. Japanese carmaker Denso plans to invest 350 million USD, taking a 10% stake in TSMC’s Japan factory expansion to revive the halted production lines. Taiwan’s Foxconn, Apple’s biggest iPhone assembler who has been seeking to have its own semiconductor capacity for years, and is in discussion with Saudi Arabia and the United Arab Emirates authorities to jointly construct a 9 billion USD foundry for microchips and other electronic components. Similarly, the American automobile company Ford is currently dependent on Taiwan’s TSMC for supplying older technology chips, but has lost its prioritized position and faced a serious chip crisis. To tackle its short- and long-term supply shortage, Ford partnered with GlobalFoundries to initially produce chips for Ford, but later also boost chip production in the U.S. Those strategies are aligned with governments’ semiconductor production localization initiatives in multiple countries.

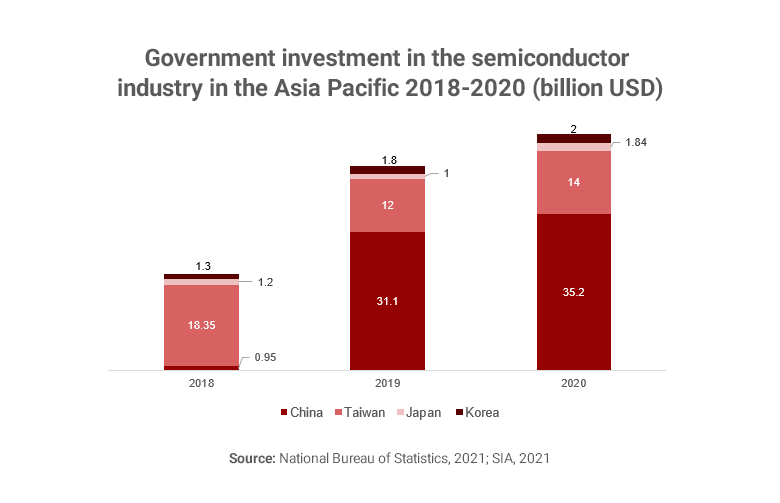

To mitigate the risks of future shortages, local governments focus on expanding production capacity and having their own semiconductor manufacturing setups in their countries or regions. The U.S, the European Union, and the Asia Pacific region are encouraging local companies to build or expand their facilities locally, or to attract FDI investments in the semiconductor sector. In the Asia Pacific region – the hub of chip production – governments play an essential part in promoting the semiconductor sector. The Chinese government’s investment in the semiconductor industry increased dramatically from less than 1 billion USD in 2018, to more than 30 billion USD in the following two years respectively, proving the Chinese government’s fierce determination to achieve self-sufficiency in semiconductor production for mainland China. The South Korean government collaborates with local companies to invest 450 billion USD to establish the world’s largest semiconductor industry supply chain. Japan has also built a fund of 1.63 billion USD for the semiconductor industry and has planned to extend support policies to attract foreign investment in advanced technology.

Despite the positive outlook and ambitious initiatives, increasing the supply capacity and localization of production is a slow process. It takes many years, billions of dollars, and lots of skilled labour to build a new semiconductor factory. In addition, semiconductor technology has been developing quickly and the demand for cutting-edge chips needed in new technologies such as smartphones and 5G devices continues to surge. Meanwhile, only a few companies can produce such advanced chips, and building those factories takes even longer time and effort. Nevertheless, companies’ and governments’ current efforts can help relieve the intense demand for electronic chips, shorten lead times and eventually reach a balanced state of supply and demand in the next two years.

To summarize, the semiconductor shortage, particularly for cutting-edge chips, is expected to linger through 2022 and most likely to 2023, with longer lead times, delayed shipment, and higher costs. It is primarily fuelled by fast growth in demand and disrupted supply chains. The shortage will affect companies to different extents, depending on the industry and application they operate on. Therefore, every company should thoroughly analyze and assess risks at all levels of its supply chain to minimize the impacts on production.

Read more about our technology sector experience or our other consulting services.

The insights provided in this article are for general informational purposes only and do not constitute financial advice. We do not warrant the reliability, suitability, or correctness of the content. Readers are advised to conduct independent research and consult with a qualified financial advisor before making any investment decisions. Investing in financial markets carries risks, including the risk of loss of principal. Past performance does not guarantee future results.

The views expressed herein are those of the author(s) and do not necessarily reflect the company's official policy. We disclaim any liability for any loss or damage arising from the use of or reliance on this article or its content. ARC Group relies on reliable sources, data, and individuals for its analysis, but accuracy cannot be guaranteed. Forward-looking information is based on subjective judgments about the future and should be used cautiously. We cannot guarantee the fulfillment of forecasts and forward-looking estimates. Any investment decisions based on our information should be independently made by the investor.

Readers are encouraged to assess their financial situation, risk tolerance, and investment objectives before making any financial decisions, seeking professional advice as needed.